Budgets for Chapters 7 and 13 bankruptcy include expenses that are acceptable by the trustees and judges. However, those expenses must make sense for your needs and income. Budgets for a Chapter 7 bankruptcy need to support the conclusion that you have no money left over after your reasonable and necessary expenses to pay a Chapter 13. It is allowable for you to take necessary and reasonable expenses so you can continue to live in a normal home and drive a normal car to work.

How to Develop Budgets for Chapter 7 and 13 Bankruptcy

If you are a doctor making $800,000 a year perhaps a new Lexus is reasonable so you can get back and forth to work to save lives. But if you make $50,000 a year, a new Lexus is not reasonable. Of course, a $175 per month Chapter 13 payment is not what the doctor will repay either. Instead, you can expect the doctor’s Chapter 13 payment to have a much larger mortgage and other expenses.

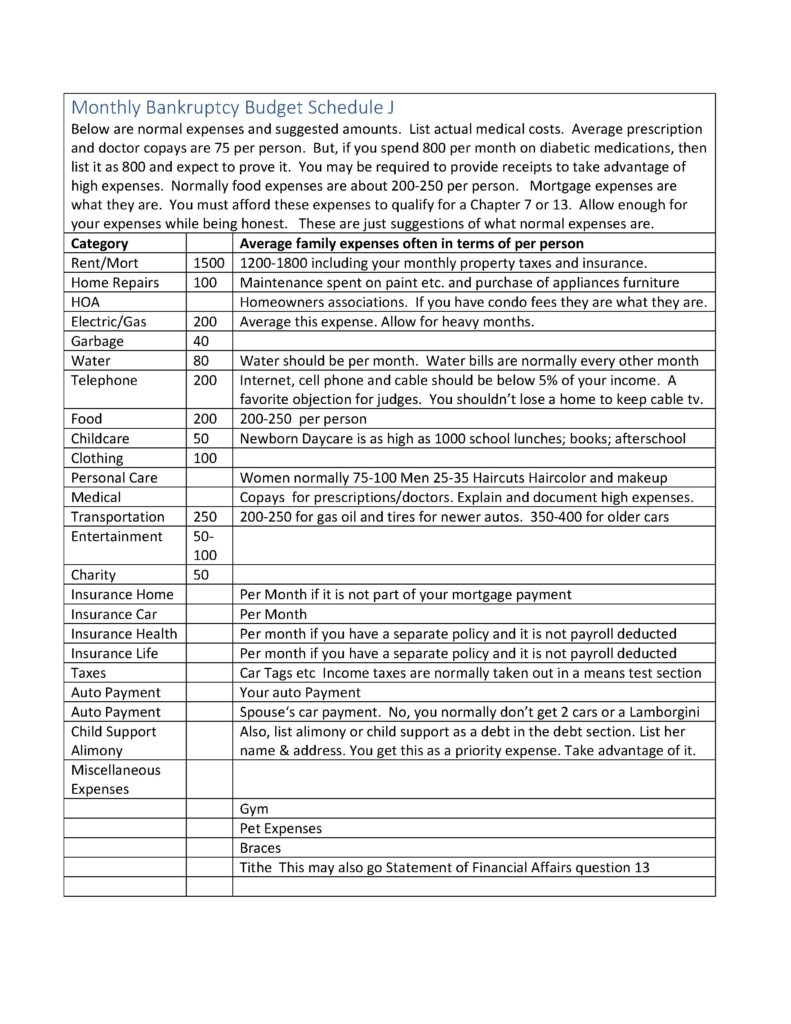

Our sample family budget is at the bottom of this post. Here it is in a pdf format for your convenience: Monthly Bankruptcy Budget Schedule J. It also includes the average allowed expenses for a normal family. But, each case is different. Therefore, the bankruptcy court and the trustee generally trust your expenses but they require you to document them. So, if you really do spend $1,000 per month on daycare, the court will allow the expense. But you may have to give them proof of this expense such as a bill for the daycare or checks to your neighbor for the daycare she is providing while you are at work.

⎆ Developing Your Budget for Chapter 7 Bankruptcy

In order to qualify for Chapter 7, your expenses must leave you with just enough money to repay the home mortgage and auto loans but not enough to enable you to repay a Chapter 13 payment. Your monthly income is your prior six months of income divided by 6. Note you do not include your current month of income. This is what is used for your means test income. If your income is less than the average monthly income for the same size family you automatically qualify for Chapter 7. But you may still qualify for Chapter 7 if your normal and reasonable expenses still leave you little or nothing in your budget to repay a 13.

You are allowed to deduct normal and reasonable expenses but not luxury items. Normal and necessary contributions include items such as paying for expenses that other people don’t need but you do. If your children are in daycare you have to budget for that expense and it goes into the child care expense of the miscellaneous expense category. If your child needs special educational training you may qualify for private schooling. You are allowed to have contributions to your 401k and many other expenses. So, look at the budget below for what the standard expenses are in addition to other expenses.

⎆ Qualifying Budgets for Chapter 13 Bankruptcy

If you want to file as a Chapter 13 your expenses must show paying something back to your unsecured creditors is possible. But you might not be able to repay very much. Budgets with repayments as low as 1% and 0% can be approved. But the Debtor has a duty to pay back as much as he can. Interestingly, if the debtor is not making any attempt to tighten their belt the judge will reject the Chapter 13 plan. Two of our judges automatically approve 50% of the plans. The other judge will automatically approve 70% of the plans.

A Chapter 13 plan requires you to repay your priority debts back and get them up to date. This includes taxes less than three years old and it includes alimony and child support. It also includes the home and mortgage be caught up if you are keeping the car or mortgage. So your budget might mean you will only be able to eat Ramen noodles for five years if you want to drive your Lexus to work.

Chapter 13 also needs to pay back as much as Chapter 7 would. If your exemptions do not allow you to keep that Lexus because you have $10,000 too much equity then a Chapter 13 which pays back $10,000 to the unsecured debts allows you to keep that Lexus or home which you may otherwise lose. The official form for the budget is schedule J. Again, the overall allowed expenses are below.

⎆ Chapter 7 & 13 Bankruptcy Budget Schedule J • Normal Expenses and Suggested Amounts

Louisville Kentucky Bankruptcy Forms

Why Review a Chapter 13 Schedule of Allowed Claims?

How to Qualify for a Chapter 7

Including Income, Assets, Debts, and Expenses in a Bankruptcy

If you are thinking about filing bankruptcy, don’t delay because timing is crucial. I am here to help you. So, contact my office right away to start the conversation. Nick C. Thompson, Bankruptcy Lawyer: 502-625-0905.