Early Discharge for Chapter 13 Bankruptcy • Video

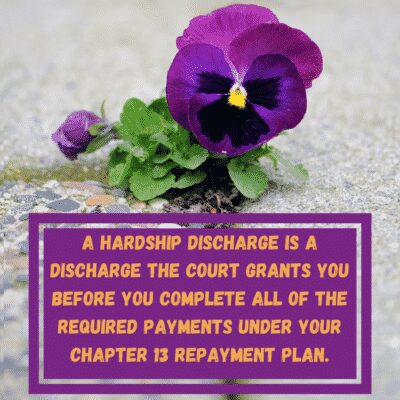

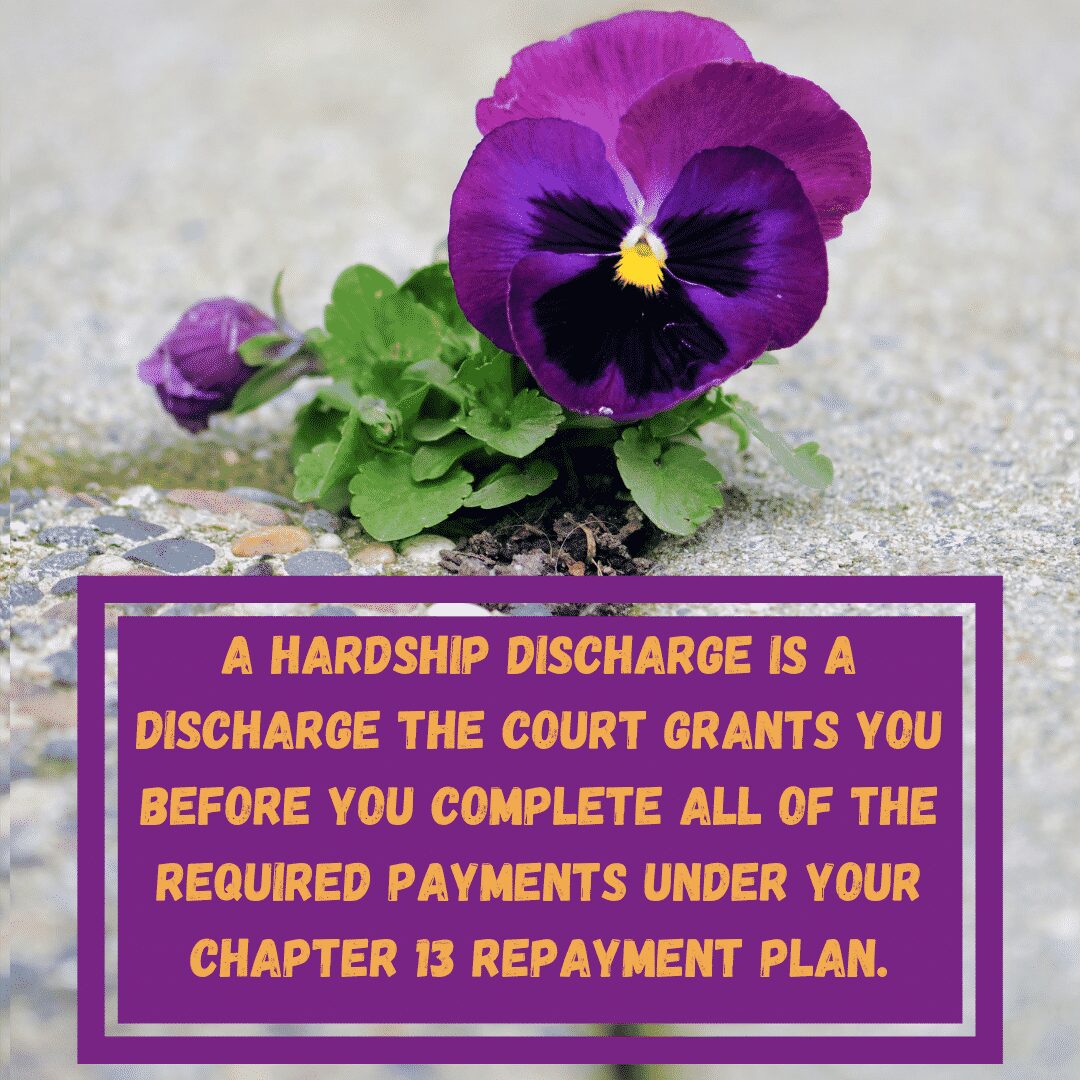

If a Debtor makes the majority of his plan payments in the Chapter 13 plan but can not continue to make payments due to no fault of his own, he may ask for an early or hardship Chapter 13 bankruptcy discharge. The words Hardship Discharge just like inside the plan are not in the code. However, all discharges come from 11 USC 1328(b). What’s interesting is if you read this section, it looks like you could ask for discharge the day after you file.

Hardship and Early Discharge for Chapter 13 Bankruptcy

Generally, our court does not allow an early or hardship discharge until after three years of payments. Additionally, the Debtor cannot be the cause of his problems and then complain about how he cannot complete the plan. Also, the debtor must give it his best efforts to complete the plan.

Entering into a status of disability is the classic cause of a Hardship-Early discharge. But, unemployment the month after you file is not a basis for this type of discharge. Conversely, the closer the case is to the end the easier it is to get an early discharge.

However, if the debtor receives a disability status, an early discharge is often allowable. But, if the debtor simply quits his job, there is no early discharge available. However, modifying a plan or suspending plan payments is the proper way to cure short-term job loss.

Moreover, if you buy a car without court approval and then can’t afford Chapter 13, you won’t get the early discharge.

⎆ The liquidation test in early discharge for Chapter 13 bankruptcy.

⎆ The liquidation test in early discharge for Chapter 13 bankruptcy.

To get the discharge in Chapter 13, every case must pass a liquidation test. What this means is the Chapter 13 must repay as much as if it were Chapter 7 filing. If the Debtor loses a diamond ring worth $5,000 in Chapter 7 because he did not have enough exemptions, then his Chapter 13 must repay at least $5,000 dollars. That’s based on the fact that the case would have repaid $5,000 as Chapter 7. In addition, the motion must include the liquidation test as an exhibit.

⎆ Temporary suspension of payments.

However, if the debtor simply needs a short period he must ask for a temporary suspension order.

⎆ Request for plan modification.

Or, if the debtor needs lower payments, the debtor must ask for a plan modification. One common example is short-term maternity leave.

⎆ Chapter 13 Plan Modifications

Debtor’s payments can increase or decrease under a plan modification. The requirement for Chapter 13 is to include payment for all of the debtor’s disposable income. But, remember, hiding income or the failure to turn over a tax refund might prevent a discharge.

However, if the debtor’s income is lower, you may lower the plan payments. Chapter 13 can also be converted to Chapter 7. But, please note that the plan can also increase if the debtor obtains a higher paying job. So, the plan is very flexible and can include increasing or decreasing payments over time in a step plan.

A debtor normally can’t pay off the plan early because rules require the debtor to commit all of his disposable income. However, there is no requirement for a debtor to pay more than 100%. If you earn less than the average income, you may have a 36-month plan. If you earn over the average wage, you must have a 60–month plan. Rather, it is far easier to file a new budget and ask the court to reduce or suspend plan payments rather than obtain an early discharge. Additionally, a debtor can always increase the plan from 36 months to 60 months.

Resources for Bankruptcy

Resources for Bankruptcy

Louisville Kentucky Bankruptcy Forms

How to Qualify for Chapter 7 • Video

Means Test Qualifying for a Kentucky Chapter 7 • Video

What is the Student Loan Brunner Test?

Chapter 13 Bankruptcy in Louisville Kentucky

Avoiding Foreclosure with Bankruptcy

Mortgage Modifications • Foreclosure Failures

If you are thinking about filing bankruptcy, don’t delay because timing is crucial. I am here to help you. So, contact my office right away to start the conversation. Nick C. Thompson, Bankruptcy Lawyer: 502-625-0905.