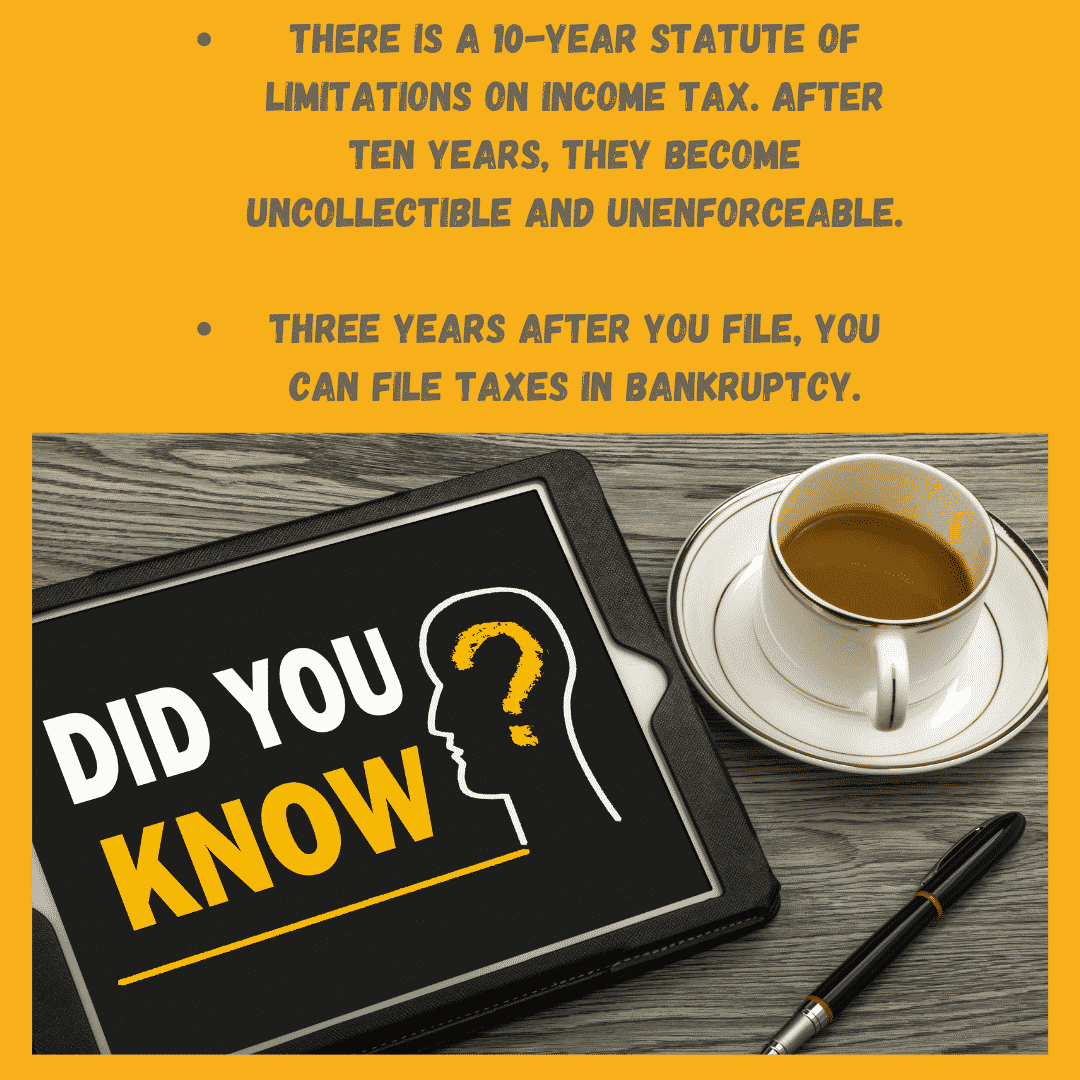

How do you bankrupt income and trust taxes. You may want to use tax discharge determinator to ensure you have calculated all the dates. Well, to begin, you know that your taxes fall due every year around Easter. So, when you file your taxes on time, the discharge tax debts are dischargeable about three years after the return’s original due date. You can contact tax discharge determinator for more information about how to calculate the right date. Periods of time like how long and when you were in a prior bankruptcy or submitting an offer in compromise may extend your waiting periods. Missing the date when you can discharge the tax is fatal to discharging your taxes. You need to know the return policy. Using the tax discharge determinator software can help you determine the date for discharging income taxes.

Additionally, the returns must be filed at least two years before filing for bankruptcy. Plus, there must be no assessment at least 240 days before filing the bankruptcy. There also must be no effort to evade the tax. This is similar to tax fraud, but courts are strict about disallowing even minor acts to avoid paying the tax. A tax discharge determination can be extremely helpful in resolving your issues if the goal of your bankruptcy is to discharge income taxes.

How to Bankrupt Income and Some Trust Taxes?

You must also be aware that some or many tax resolution companies are expensive scams. They will attempt to get you a payment arrangement or attempt to file an offer in compromise but because they are not a law office they can’t offer you the option of simply bankrupting your taxes. Most bankruptcy attorneys can not name the five significant steps to discharge income taxes. The IRS will offer you a payment plan to solve your tax problems or they will accept an offer in compromise but they will never suggest to you that you can bankrupt the tax debt and repay them nothing. Do not expect any help from them.

IRS collections

Many attorneys do not have the knowledge I have from working for the tax department. The IRS Insolvency unit and IRS collector can be brutal in collections.

The critical thing to note is that the rules are difficult to understand. For instance, calculating the earliest date when taxes are dischargeable requires a copy of your tax account transcript to see the date the service received a copy of your return and other events in your record. It can take hours with the tax codes if you have to determine by hand whether there was an assessment or other event that would change the earliest date you have to file.

Remember, trust and property taxes are generally not dischargeable. But, don’t assume that they cannot be discharged. The part of trust taxes the business pays may be dischargeable when you hire a tax discharge determinator, following the step-by-step rules below to establish when you can successfully bankrupt taxes.

Bankruptcy and Tax Planning

Income and some trust taxes are dischargeable in bankruptcy. Trust taxes are often the withholding and sales taxes you hold for the tax department. Business owners have no ownership rights and only hold these trust tax funds for the department. Spending these funds can be a felony in Kentucky. Bankrupting income taxes or the dischargeable portion of a trust tax is essentially a waiting game. Taxes must age like wine until they are old enough to be dischargeable. And, only a couple of methods work. You can offer the IRS a payment plan and age your taxes but an offer in compromise does not work.

You generally cannot calculate when the return is old enough unless you have the tax account transcript and tax codes. The account transcripts show when an assessment is made, audit information, when the return was received, and when you make an offer in compromise or asked for a due process hearing. It is the complete history of your account. Your tax account transcript is not your tax return.

Go here to learn how to get your IRS Tax Transcript. Accurately determining your tax dischargeability is complex, and the account transcripts are recorded in code. That’s why you need a tax and bankruptcy attorney with the qualifications to help you plan either a repayment plan, offer in compromise, bankruptcy or abatement to discharge the tax. This isn’t easy. To get started, come see us to calculate when a tax is old enough to discharge in bankruptcy.

How to Bankrupt Income Taxes in 5 Steps

1: Taxes Must be 3 Years old to be Dischargeable under 11 USC 507 (A)(8)(A)(i)

If your return was due to be filed on October 15th, 2020, because you filed an extension, you have to wait three years later after that. They generally became dischargeable on October 15th, 2023. However, this rule is not perfect. Since April or October 15th may have fallen on a weekend, you should add ten days to ensure. Miss the date by one day, and you will owe the tax. You can repay income taxes in Chapter 13 but miss this date and you owe 100% of the tax as a priority debt which must be paid 100% in full during the Chapter 13 plan.

2: Returns Must be Filed Over 2 Years Before You File Bankruptcy 11 USC 523 (A) (1) (b)

This period never starts if the return is not filed and signed by the taxpayer. This 2-year rule is an essential requirement. The IRS Insolvency Unit must have this 2-year opportunity to collect. Filing a signed and accurate return under oath starts the 2-year waiting period for the tax to be discharged. Nothing will replace this requirement. You have a vital requirement as a business and taxpayer to keep records and report under 11 USC 523 A.

3: Wait 240 Days After Any Assessment 11 USC 507 (A)(8)(A)(ii) to File Bankruptcy

When you went through that audit, and they increased your tax debt, that was an assessment. If they were sent a 1099 because your credit card was charged off the IRS issued an assessment. There was an assessment if they sent you a supplemental tax bill for cashing your 401k. This 240-day rule does not count if the appraisal was not sent to the last known address, over three years after filing the return, the assessment was a re-assessment, or the judgment was arbitrary and clearly in error.

4: The Return Must Not Be Fraudulent or An Attempt to Avoid the Tax 11 USC 523 A 1 b and 11 USC 523 a 1 c

If you fail to file a tax return, the IRS can file a tax return for you. This is called a substitute for return. They will guess what they think you earned and they will not use any deductions. This will often be about twice your average wages and becomes your tax due unless you timely protest it. The failure to file the return, an inaccurate return, and about 20 other acts may be a “willful or negligent evasion”. They normally use “negligent evasion” because willful is more difficult to prove.

Fraud or willful evasion makes it difficult or impossible to discharge the tax in bankruptcy. If they file a substitute for return, most bankruptcy judges will never allow discharge of the income tax without payment in full. The IRS and taxpayer can file an agreed “SFR” (substitute for return) together with you. Then the taxpayer has filed a return under oath before an audit is final and the tax debts are dischargeable.

5: To Calculate the 2-year Rule Add Any period, You Were in Bankruptcy Plus 90 Days

The tax department takes the position it is unfair to them to not have at least two years to know about the income tax debt and effectively collect from the taxpayer. If you file a bankruptcy before the two years, they don’t have an “opportunity to collect.” They feel the debtor has made no reasonable effort at repayment. According to 11 USC 507 8 A (ii) (II) filinga bankruptcy is a “tolling event” that extends the 2-year rule and statute of limitations for that period plus 90 days.

Filing an Offer in compromise extends the 240 days rule the period you were in an offer in compromise application plus an additional 30 days. An offer in compromise is also a “tolling event.” I always add an added 10-day period just for safety period just in case the date falls on a holiday or weekend or the mail is slow.

Age a Return to Discharge the Tax

If you need to age the return to discharge the tax, you may want to enter into a payment arrangement. Using an offer in compromise or filing a bankruptcy stops the clock from running on the statute of limitations. Often payment agreements can be for less than the interest on the income tax debt.

If you are very poor, the tax department may place you into a currently uncollectible status which also ages the account. If you can age the return to make it dischargeable, the IRS may claim you need to sign form 656. This form prevents the account from aging. Never sign this form. It is never required. You want the clock to run out on them. The IRS has no obligation to tell you the truth. Believe it or not they have said that in lawsuits in tax court and the Tax court has agreed with them. They are not responsible for their own bad advice. In fact every year the agents are given a test and half of them fail.

Statute of Limitations for Tax Collection

According to 26 USC 6503, tax liens self-release ten years after the date of assessment. It requires a signed tax return for the tax to be “assessed”. This statute of limitations does not apply to a fraudulent or non-filed return. Filing bankruptcy extends the statute of limitations to the period you are in bankruptcy plus six months. This means file your return on time or you may forever owe the tax.

How to Bankrupt Trust Taxes?

Trust taxes are primarily the withholding and sales income taxes merchants should hold in trust for the tax department. The Trust portion of a Trust tax is not ordinarily dischargeable under 11 USC 1328 a and 508 8 D. Notice I said usually. Every situation is different. There are exceptions to every rule. If you are an employer and failed to turnover withholding, you are stuck for the employee portion of the trust tax.

The employer portion is dischargeable since it was not held in trust. Same with sales taxes for the non purchaser portion of the sales tax. ONLY THE TRUST PORTION of a 940 trust tax is nondischargeable. The other part can be discharged in bankruptcy. In some states, the sales taxes are the seller’s responsibility and are therefore dischargeable. In Kentucky, the merchant holds the sales tax in trust and it is not dischargeable.

The interest and penalties can be eliminated for the unsecured or non-priority portion of tax debts. This eliminates half or more of a trust tax debt the IRS is requesting. You can take up to 5 years to repay secured and priority taxes which will have an interest. Dischargeable trust taxes use the same rules you use to discharge income taxes.

Miscellaneous Tax and Bankruptcy Rules

If you want to file bankruptcy like a pro, download our free book on bankruptcy. In Kentucky and Southern Indiana, see our file for bankruptcy. Income Taxes become due normally on April 15th. But some years like 2020 this date is delayed, falls on a weekend, or falls on a holiday. Believe it or not, one year they made up a holiday for that date. That is why I always add a couple of days to prevent that error.

Real Estate property taxes are statutory liens. They can’t be stripped in bankruptcy because you didn’t consent to them. Real Estate property taxes are rarely collected personally from the individual. But it is possible in Kentucky. The State tax department has purchased tax liens and ordered them in severe cases.

Nick is a former tax department prosecutor with license # 51 before the United States Tax Court in Washington DC.

Contact Us to Know More About Discharging Taxes!

Being an experienced bankruptcy attorney in this field, you can get every detail by contacting Nick. We pledge to guide our customers till getting the desired discharges for both trust and income taxes.

Helpful Links for This Article:

Resources for Bankruptcy

Resources for Bankruptcy

Tax and Bankruptcy Lawyer for Business Trust and Income Tax • Video

File Bankruptcy on Income Taxes • Video

Bankruptcy Filing Time Limitations

Tax and Bankruptcy Lawyer for Business Trust and Income Tax

Chapter 11 Business Bankruptcy Information

Student Loan Collection Defense Lawyer

If you are considering bankruptcy, don’t delay because timing is crucial. I am here to help you. So, contact my office immediately to start the conversation—Nick C. Thompson, Bankruptcy Lawyer: 502-625-0905.